SK Hynix - A Deep dive

The most critical AI company you’ve never heard of (and looks ridiculously undervalued)

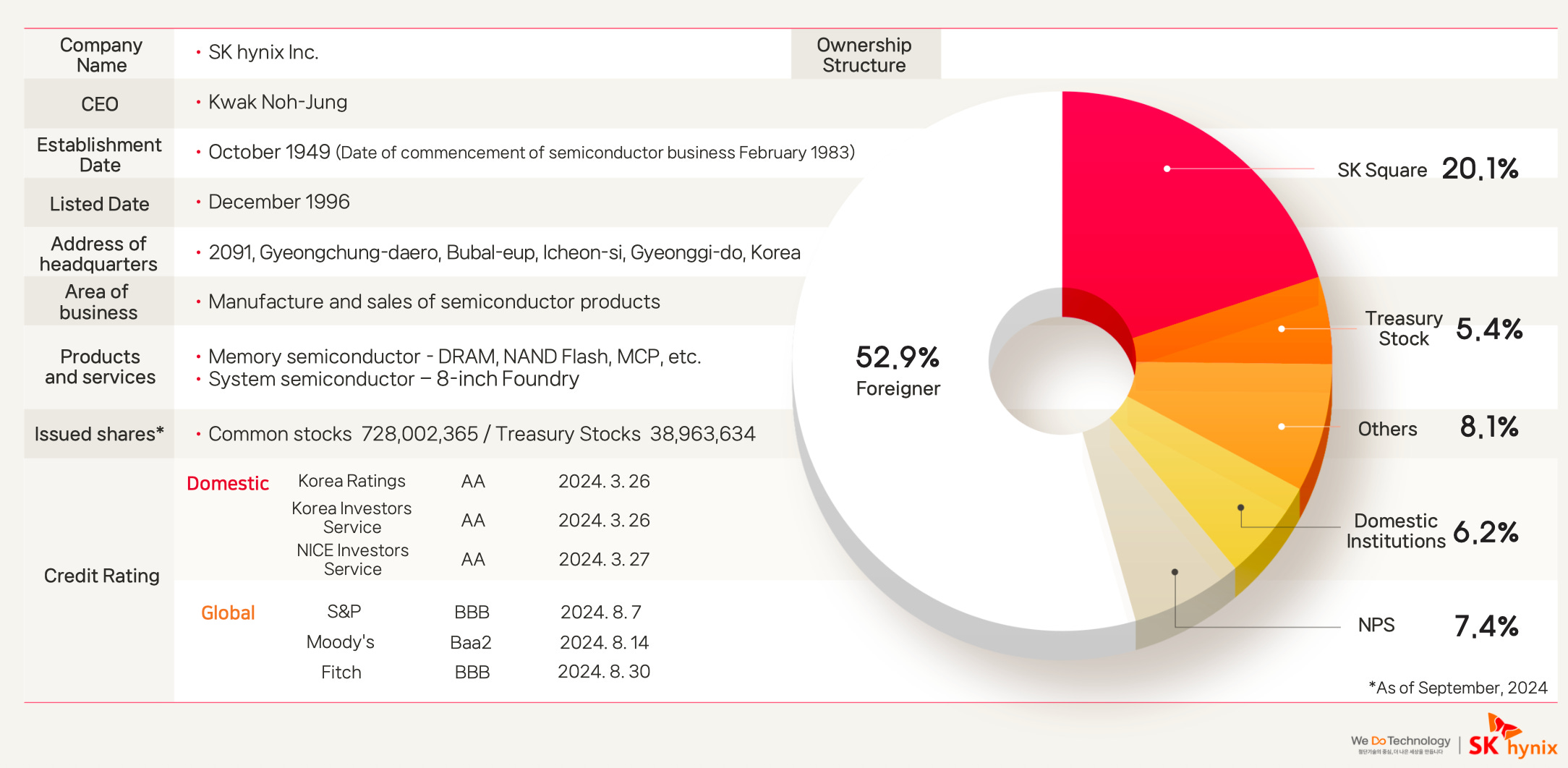

Company Overview

History and Evolution

Founded in 1983 as Hyundai Electronics, SK hynix is headquartered in Icheon, South Korea. The company survived the brutal Asian Financial Crisis of the late 1990s through aggressive restructuring, emerging in 2001 as Hynix Semiconductor.

The real transformation came in 2012, when SK Group, South Korea’s second-largest conglomerate, acquired the company for ₩3.4B. SK Group provided deep capital reserves, long-term vision, and the institutional stability needed to make significant technology bets. Under SK’s backing, the company became SK Hynix and began the decade-long investment in HBM technology that would eventually make it indispensable to the AI revolution (we will get there later).

Shareholders and CEO

There’s practicaly no insider ownership as management holds less than 1%. The largest shareholder is SK Square, SK Group’s investment holding, with approximately 20%. Although the management doesn’t have significant “skin in the game,” it is reassuring that the holding company maintains a strong interest in the business. The rest trades freely, with foreign institutional investors holding over half the company.

Kwak Noh-Jung has been the CEO since February 2022. He has been with the company for 26 years, joining Hynix (prior to the SK acquisition) in 1998 as an engineer. He spent most of his career in DRAM development and product planning, eventually rising to executive VP of DRAM Development before being appointed CEO. Kwak holds a degree in Electronics Engineering and is known internally for his deep technical expertise.

To understand SK Hynix’s business, we first need to understand everything about memory (chips, not ours).

Types of memories

NAND - Slow, Cheap, Permanent (The archive)

When we save a photo or download an app, that data needs a permanent home, that’s the job of NAND. This type of memory is the silent hero inside our smartphones, laptops (those who use SSDs), and every memory card we own. A key point is the fact that it’s non-volatile, meaning the data stays safe even when we turn off the power.

This memory is the slowest but also the cheapest, which is why it’s used to store large amounts of data. However, there’s a drawback: NAND is relatively slow at delivering data to the CPU. The flash cells used in NAND require milliseconds to access, and the amount of data it can provide at a time is limited compared to other types of memory. For these reasons, we need faster alternatives.

DRAM - Fast, Volatile, Essential (The workspace)

Think of DRAM as the essential short-term memory of every piece of digital technology. It’s the high-speed active workspace where our computer, smartphone, or smart TV temporarily keeps all the information it needs for immediate use.

When we’re simultaneously scrolling through social media, streaming a high-definition video, and downloading a file, our device is constantly accessing DRAM to sustain smooth, continuous operation. What makes DRAM faster than NAND isn’t just that it can deliver more data, it’s fundamentally different technology. DRAM uses capacitors that can be accessed in nanoseconds, compared to NAND’s flash cells that require milliseconds (looks small, but actually makes the diference).

Take DDR5, for example. It uses a 64-bit per module at speeds ranging from 4,800 to 6,400 MT/s (megatransfers per second), delivering approximately 38-51 GB/s bandwidth per module. That’s a massive upgrade over NAND.

But there’s a trade-off. DRAM, on the other hand, is volatile, meaning its data is lost the moment power is removed. Despite this limitation, it’s indispensable due to its exceptional speed. This necessity for speed makes the technology inherently complex and expensive.

Yet even with DRAM’s impressive performance, relying solely on it would still leave your computer feeling sluggish. That’s where the last piece comes in, SRAM.

SRAM - Smallest, Fastest, Priciest (The drawing)

SRAM is an extremely fast memory and is the only one built directly inside the CPU or GPU which means it’s also rather small. Despite its limited capacity, we absolutely need it. SRAM holds tiny amounts of data that the processor needs immediately, this is what we call cache (L1, L2, L3, etc.). No modern processor can function without it, as cache prevents the processor from constantly waiting on slower external memory (DRAM).

Here’s the challenge: SRAM is physically large and expensive to manufacture. Each bit requires six transistors, compared to DRAM’s single transistor and capacitor. This is why cache is measured in mere megabytes, typically just 32-128 MB across all cache levels, while DRAM can be hundreds of gigabytes.

That’s why every system needs DRAM as the main memory. It’s slower than SRAM but provides the massive capacity needed for all active applications, residing as a separate chip outside the CPU/GPU. Like DRAM, SRAM is also volatile, losing all data when the device powers off.

The AI Revolution and the Birth of HBM

Artificial intelligence created an immediate engineering challenge for the tech industry. Modern AI relies on GPUs, which can process massive amounts of data in parallel, far beyond the capabilities of traditional CPUs. The problem was that conventional DRAM couldn’t feed these GPUs fast enough. Picture a motorway with ten lanes, but only two are open: GPU cores, despite their enormous processing power, were often idle, waiting for data. The industry needed a radical solution to unlock the full potential of GPUs.

The answer was High-Bandwidth Memory (HBM), a specialized DRAM architecture that transformed GPU performance and AI workloads.

How HBM Works

Traditional DRAM is laid out flat, limiting bandwidth and creating a bottleneck for high-performance computing. HBM solves this with three key innovations:

3D stacking: DRAM chips are stacked vertically, currently up to 12 layers high (will probably increase in the next few years), with taller stacks planned. Thousands of microscopic Through-Silicon Vias (TSVs) carry power and data directly through the stack, creating a massive data superhighway in a small footprint.

Ultra-wide interface: While DDR5 DRAM uses a 64-bit at approximately 6,400 MT/s (~51 GB/s per channel), HBM uses a 1,024-bit operating at around 9.6 Gbps per pin, delivering roughly 1,200 GB/s per stack, 20–25 times faster than a single DDR5 channel. With 8 stacks, this translates to approximately 9,600 GB/s (like the HBM3e). It’s like upgrading from a two-lane road to a 32-lane superhighway.

Proximity to the GPU: HBM is mounted on a silicon interposer just millimeters from the GPU, compared with several centimeters separating conventional DRAM from the CPU. Shorter distances reduce latency and power consumption, making data transfer more efficient.

Real-World Impact

Modern AI accelerators use multiple HBM stacks for staggering throughput. Examples:

NVIDIA H200: 6 stacks → ~4.8 TB/s total bandwidth

NVIDIA B200: 8 stacks → ~8 TB/s total bandwidth

Without HBM, GPU cores might spend 70–80% of their time waiting for data, with utilisation as low as 20–30%. With HBM, utilization jumps to 80–95%, training time drops 3–5x, and inference costs fall by roughly 50%. Essentially, HBM allows GPUs to process massive amounts of data in parallel without being throttled by memory limitations.

HBM delivers 20–40x more bandwidth than conventional DDR5 while consuming less power per gigabyte transferred. It’s not just faster, it’s fundamentally more efficient, enabling AI workloads that would be impossible with conventional DRAM alone.

Why Only Three Companies Can Make It

If HBM is so critical, why don’t more companies produce it? The answer is simple: it’s extraordinarily difficult and expensive.

Only three companies can manufacture HBM at scale: SK Hynix, Samsung, and Micron. The barriers to entry are huge.

Start with the TSV technology; drilling perfect microscopic holes through silicon without damaging requires specialised equipment that few companies have. These TSVs have a pitch of roughly 40 microns (narrower than a human hair) and alignment across 12 layers must be sub-micron accurate. One tiny mistake, and the entire stack fails.

Which brings us to yield challenges. Each layer in the stack can have defects, and if a single layer fails, the entire stack becomes unusable. A 12-layer stack with 99% yield per layer results in only 87% final yield. That’s 13% of production lost to defects and that’s assuming near-perfect execution. Low yields translate directly to expensive production.

Then there’s advanced packaging. HBM requires 2.5D packaging technology like TSMC’s CoWoS (Chip-on-Wafer-on-Substrate). This involves micro-bump connections between layers at approximately 40-micron pitch and sophisticated thermal management to dissipate heat through the vertical stack.

Finally, the capital requirements are massive. Building HBM capacity costs billion of dollars. They specialised bonding equipment from a handful of suppliers who can barely keep up with demand. And even after spending billions, it takes years to qualify production and win customer trust.

This is why SK hynix dominates the market today. They made a significant bet, investing heavily in HBM while competitors hesitated. When AI exploded, SK hynix was years ahead and that lead has only widened.

The Memory Hierarchy: A Summary

So let’s bring it all together.

NAND is the foundation, slow but cheap and non-volatile. It’s perfect for storing massive amounts of data permanently in SSDs and memory cards. Built far from the processor, it serves as the long-term storage.

DRAM is the active workspace. Fast, volatile, and sitting on the motherboard a few centimetres from the CPU. DDR5 can deliver 40-50 GB/s per module, providing the capacity and speed needed for everything we’re actively working on.

SRAM is the fastest. Built directly inside the CPU or GPU as cache. Extremely expensive and limited in capacity (just megabytes), but essential for preventing the processor from waiting on slower memory.

HBM is the AI game-changer. Specialised DRAM stacked vertically with 1,024-bit and bandwidths reaching thousands of gigabytes per second. Built adjacent to the GPU via advanced packaging, it’s what makes modern artificial intelligence possible.

Each type of memory exists because no single technology can be fast, large, and cheap simultaneously. Together, they form a hierarchy that powers everything from your smartphone to the AI models reshaping our world.

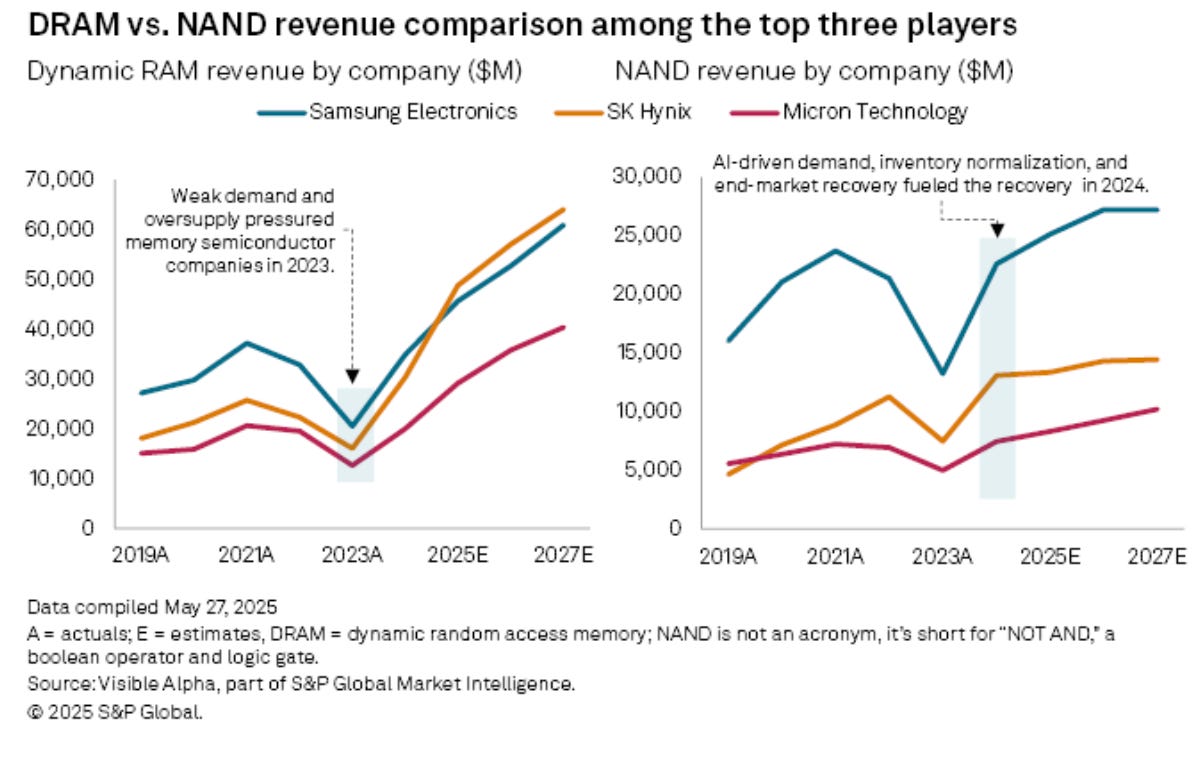

DRAM and NAND account for nearly 90% of the total memory market and this is the foundation of SK hynix.

In DRAM, SK hynix is now the global leader. In Q1 2025, they overtook Samsung in DRAM market share (with over 30%) for the first time in 30 years.

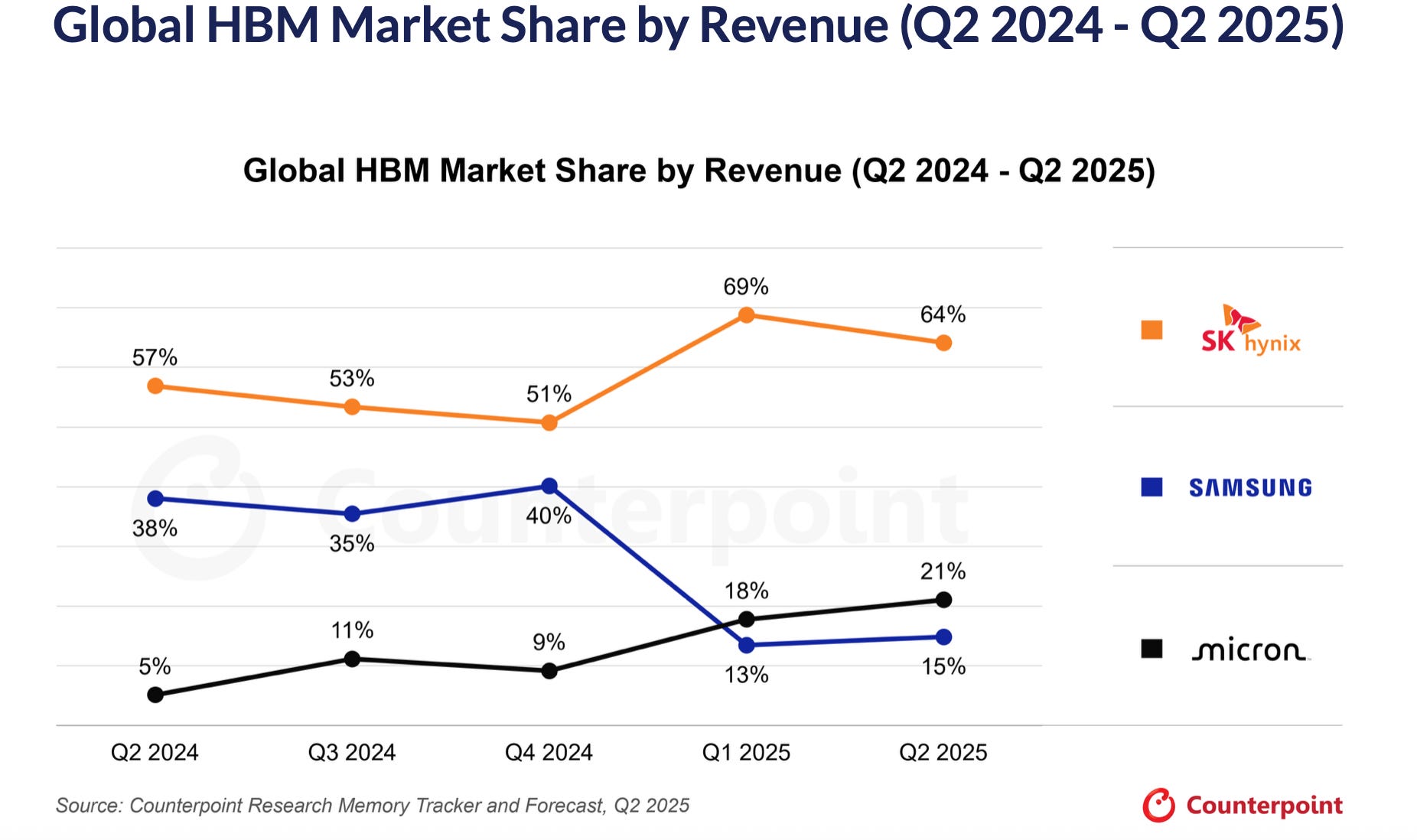

While commodity DRAM remains important, SK hynix’s leadership in HBM has transformed it from a cyclical memory manufacturer into an indispensable supplier for AI infrastructure. And its market dominance is actually growing. Despite Samsung’s aggressive capacity expansion and Micron’s steady progress, SK Hynix’s HBM market share has climbed from 57% in Q2 2024 to 64% by Q2 2025. Samsung, meanwhile, has collapsed from 38% to just 15% over the same period.

DRAM is where the money is, and HBM is where the future is. NAND is profitable but commoditized. DRAM, especially HBM, commands premium pricing with margins exceeding 40%. SK hynix’s is the dominant player in the highest-margin segment of the highest-value memory type.

NAND and the Intel Deal That Redefined SK hynix

In December 2021, SK Hynix made its biggest acquisition, acquiring Intel’s NAND and SSD business for ₩10.7T. The deal was split into two payments: ₩8.0T upfront and ₩2.7T completed in March 2025, giving birth to a new subsidiary, Solidigm.

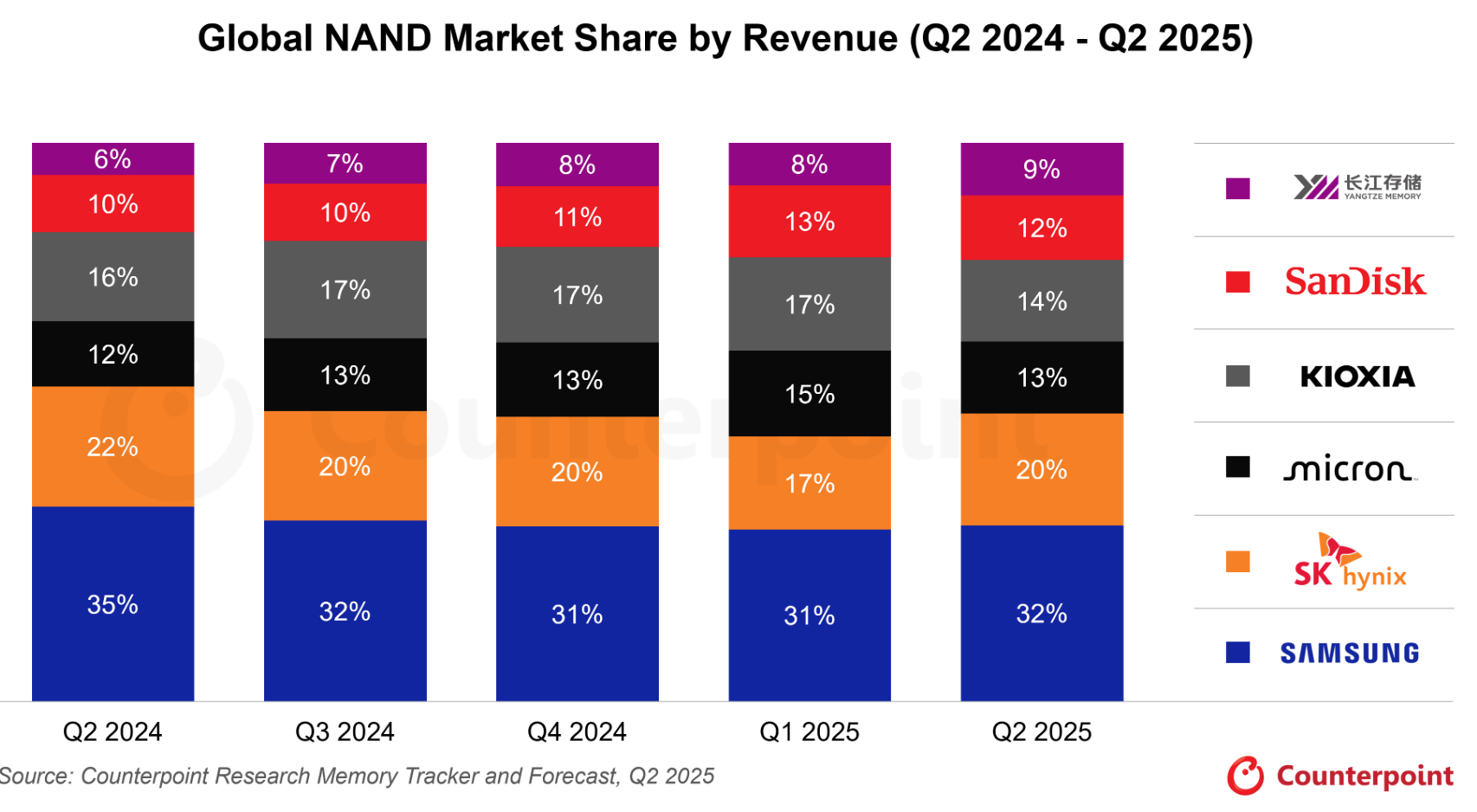

With this, SK hynix jumped from #5 to #2 in global NAND, gaining around 20–22% market share, Intel’s enterprise SSD expertise, and relationships with AWS, Microsoft, and Google. The deal was made at roughly 1.6× EV/Sales; however, the timing couldn’t have been worse. Soon after closing, the memory market collapsed, and Solidigm’s revenue plunged from ₩7T to around ₩3.3T by 2023.

The business has since stabilised near ₩4T, about 6% of SK hynix’s total revenue. Margins remain thinner than DRAM or HBM, but Solidigm is now contributing to operating profit and it’s strategically important.

More than anything, the Intel deal turned SK hynix into a complete memory company, extending its reach from DRAM dominance to enterprise storage and cloud infrastructure.

More recent data suggest that SK hynix’s market share is around 20%, behind Samsung.

AI and hyperscalers

The global HBM market is entering explosive growth, and it’s being driven by a simple reality: every tech giant is racing to dominate AI, and HBM is the fuel that makes it possible.

We’re watching hyperscalers like Amazon, Microsoft, Google, Meta spend unprecedented amounts of capital into AI infrastructure. And most of that money is flowing into two things: AI chips (GPUs) and the data centers to house them.

But there’s a big problem: there isn’t enough HBM to meet demand. Production capacity is completely sold out. SK hynix can’t make it fast enough. Samsung is trying to ramp up but facing quality issues. Micron is expanding but starting from a small base. Cloud providers are competing not just for GPU allocation but for the memory allocation inside those GPUs.

All these companies are pursuing different strategies, yet they all need the same critical component.

Meta is building AI for itself. They’re training massive models to power recommendations, content moderation, and new products across Facebook, Instagram, and WhatsApp. Their infrastructure is internal, they’re not selling AI services to anyone else. But they need just as much compute power as anyone else in the race.

Microsoft and Google are playing both sides. They’re using AI internally (think Copilot in Office, Gemini in Google Search), but they’re also major cloud providers selling AI infrastructure to other companies. They need enormous capacity both for their own products and to rent out through Azure and Google Cloud.

Amazon is the pure infrastructure play. AWS is highly focused on being the platform where everyone else builds AI. They’re constructing massive GPU clusters so that startups and enterprises can access AI computing power without building their own data centers. Every customer request translates into more HBM demand.

NVIDIA sits at the center, manufacturing the GPUs everyone wants. But even NVIDIA is constrained, they can only ship as many chips as their suppliers can deliver HBM.

Despite wildly different business models between internal AI, cloud services, pure infrastructure, they all converge on one requirement: you cannot build AI without GPUs, and GPUs cannot function without HBM.

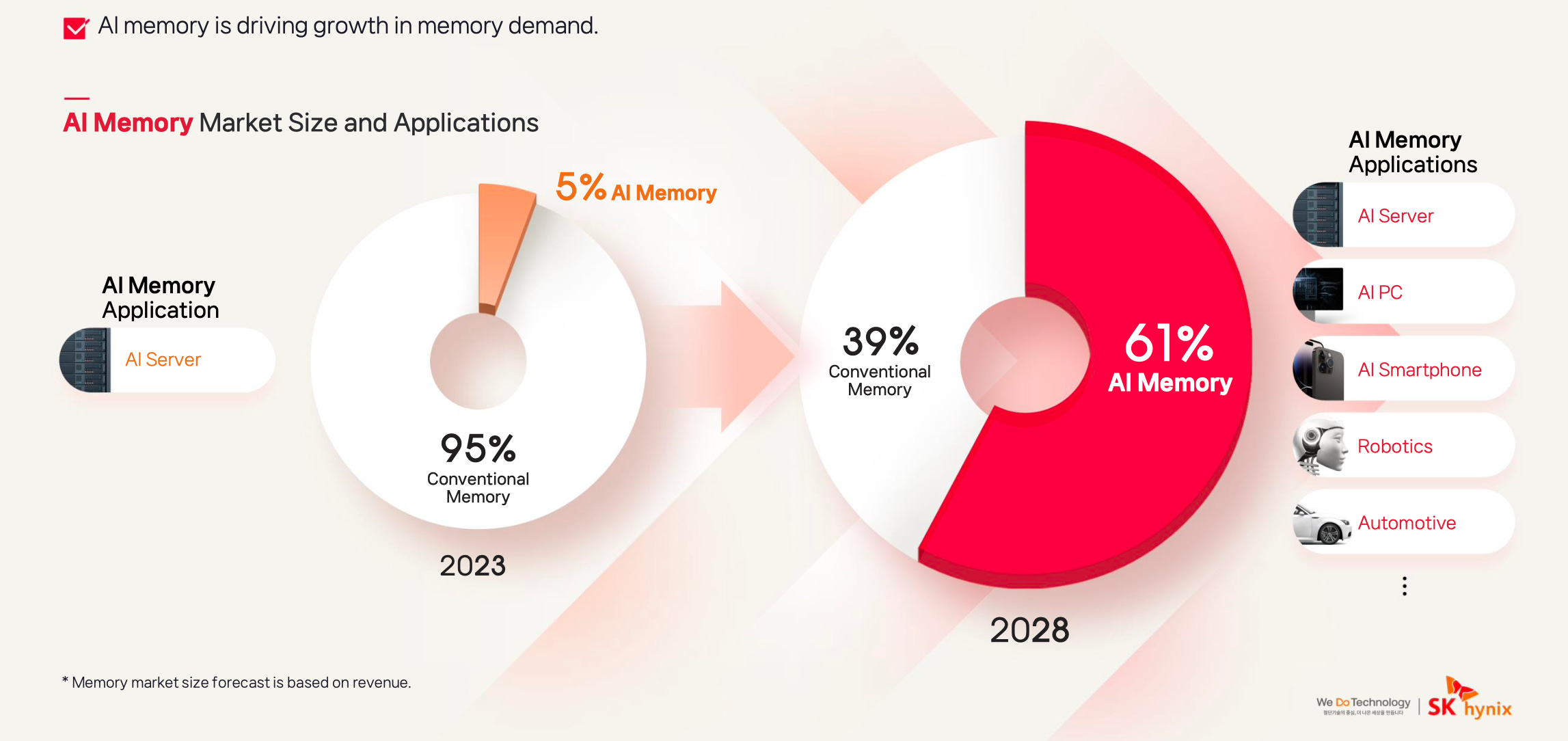

The market reflects this reality. In 2023, AI memory (primarily HBM) represented just 5% of the total memory market. By 2028, that figure is projected to reach 61%.

That’s a complete transformation of the memory industry. The market is pivoting from serving billions of PCs and smartphones to serving millions of AI accelerators. And because each AI chip requires vastly more memory bandwidth than traditional devices, HBM is becoming the dominant product in an industry that was previously dominated by commodity DRAM and NAND.

For SK Hynix, this is the payoff for a bet made nearly a decade ago when HBM was still experimental.

Cyclical industry

The semiconductor industry is highly cyclical, with significant ups and downs. It’s heavily tied to economic indicators, and being a capital-intensive business, the swings can be brutal. In good years, demand for chips grows and these companies print money. In recessions, most companies play it safe and push back on investments as chips aren’t exactly cheap. That’s when semiconductor manufacturers build up inventory and eventually have to push prices down. I suppose it’s easier to cut CapEx instead of operating expenses.

During COVID, there was massive demand for electronics like laptops, smartphones, cloud infrastructure and companies like SK Hynix increased production of NAND and DRAM, the critical components needed to satisfy that demand. As the hype faded in 2022, inflation hit, interest rates spiked demand for chips collapsed.

This has been happening repeatedly. Good times lead to growth in demand. Semiconductor companies ramp up production to satisfy it. Then the economic cycle turns. People buy fewer smartphones and laptops, leaving these companies holding massive inventories. They need to get rid of excess inventory fast because the technology becomes outdated quickly. They sell at a discount, prices crash, and the cycle starts again.

But AI seems to be breaking this pattern. With such strong growth prospects and hyperscalers who have the cash to invest regardless of the economic cycle, they’ve been significantly ramping up AI investments. If you look at the last quarterly reports from Meta, Google, Microsoft, they’re moving enormous cash flows into AI. And here’s the key and what could differentiate AI from other bubbles: they’re getting real ROI from their AI investments. AI is driving advertising revenue for Meta and Google. AI services like Azure and Gemini are generating revenue for Microsoft and Google. And we have AWS, the leader in cloud services. And NVIDIA, which designs most of the world’s high-end GPUs and whose valuation has skyrocketed, simply cannot secure enough supply to meet current demand.”

This could be like any other past cycle, like the one we had during COVID and the following years. However, AI demand appears to be somewhat independent from economic cycles, at least for now. Semiconductors aren’t just selling DRAM and NAND for smartphones or laptops anymore. They’re building and creating new technologies for something that wasn’t here before. For AI, trillions of dollars will be spent in the next few years, with significant growth rates ahead.

I know that eventually, one of two things will happen: either AI components like HBM will be commoditised as more companies catch up to SK Hynix’s technology, or demand for AI will slow down. I believe both will happen eventually, however the technology is so complex that I don’t see any other company, especially outside the three giants SK Hynix, Samsung, and Micron getting anywhere near the technology quality that SK can offer. And from what we’ve been seeing, I don’t see demand for AI stagnating in the next 5 years.

That said, DRAM and NAND are already somewhat commoditised. But HBM, the critical, cutting-edge technology that offers is years away from being commoditised. The technology gap is just too wide.

Operating results

SK hynix operates four major production sites, heavily concentrated in South Korea. The flagship facilities are Icheon (highly focused in the HBM) and Cheongju (DRAM and NAND), with Bundang serving as the primary R&D center.

Beyond Korea, the company maintains two facilities in China, Wuxi (DRAM production) and Dalian (Solidigm’s NAND manufacturing).

The global footprint includes R&D centers, sales offices, and four key affiliates (Solidigm, Dalian semiconductor, Wuxi System IC, and SK Key Foundry) representing non-core operations outside the main memory business.

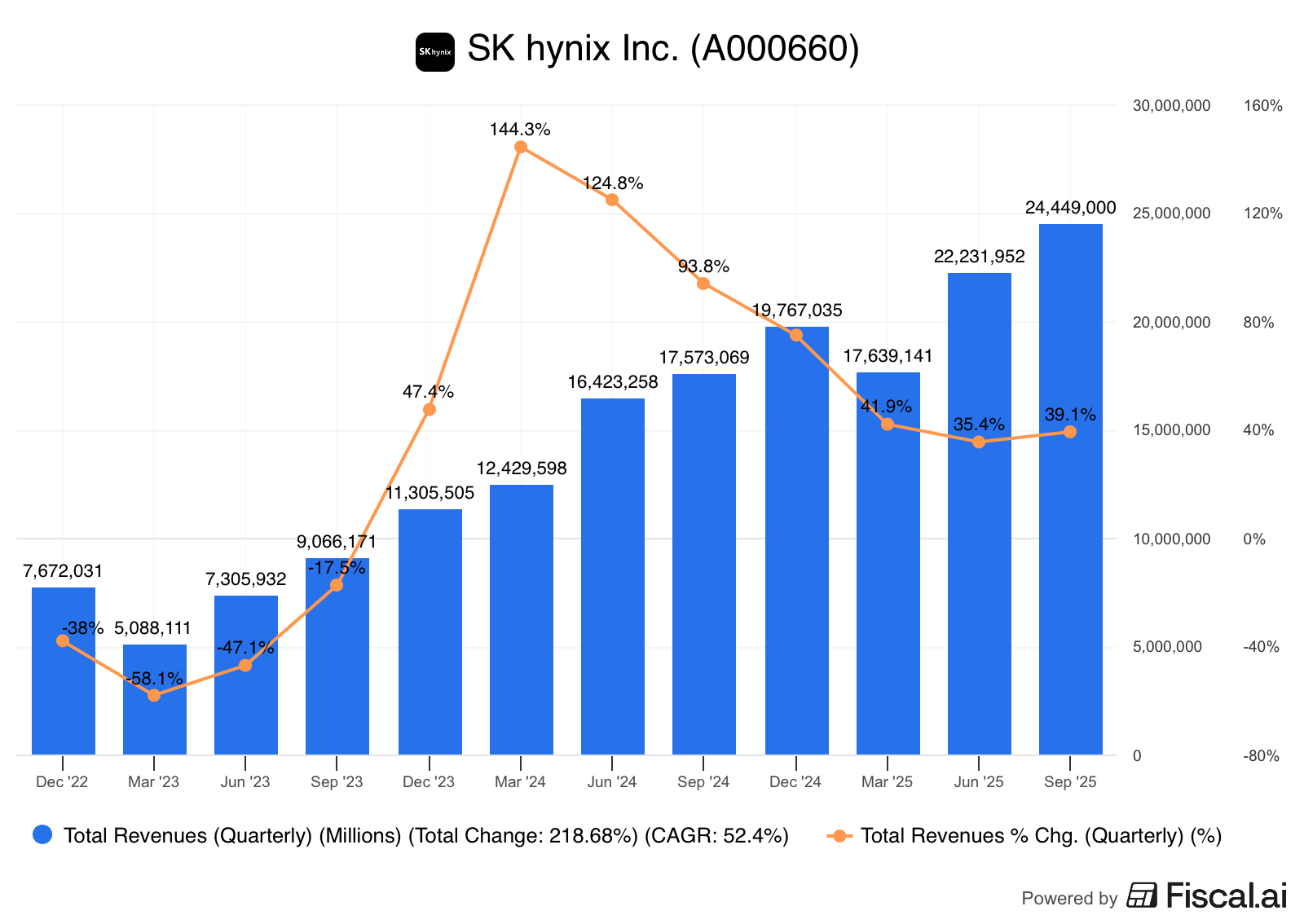

Revenue

Revenues have risen almost every quarter. While the top line grew at over 50% CAGR for years, growth has recently stabilised at a still impressive 35-40% YoY.

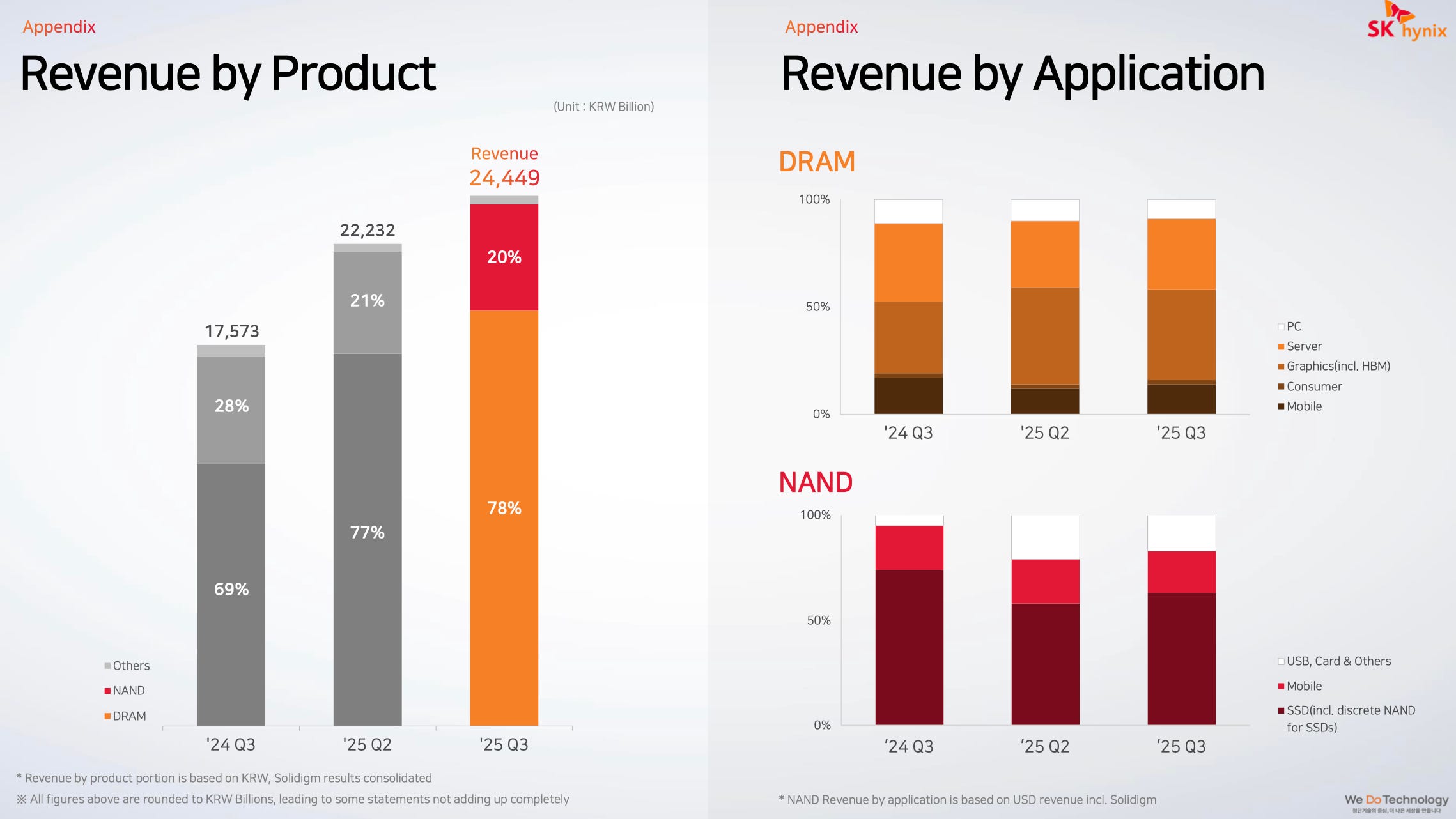

As expected, DRAM is responsible for almost 80% of revenues, with HBM taking a significant portion of this revenue. NAND accounts for just 20%. Looking at revenue by application, most of the DRAM is going toward servers and graphics. These two applications dominate DRAM demand because servers require massive capacity and reliability for operation, while graphics demand higher speed and bandwidth to handle the immense parallel processing of modern gaming and AI models. NAND, on the other side, is primarily going toward SSDs, with USB drives and cards becoming more relevant in recent quarters.

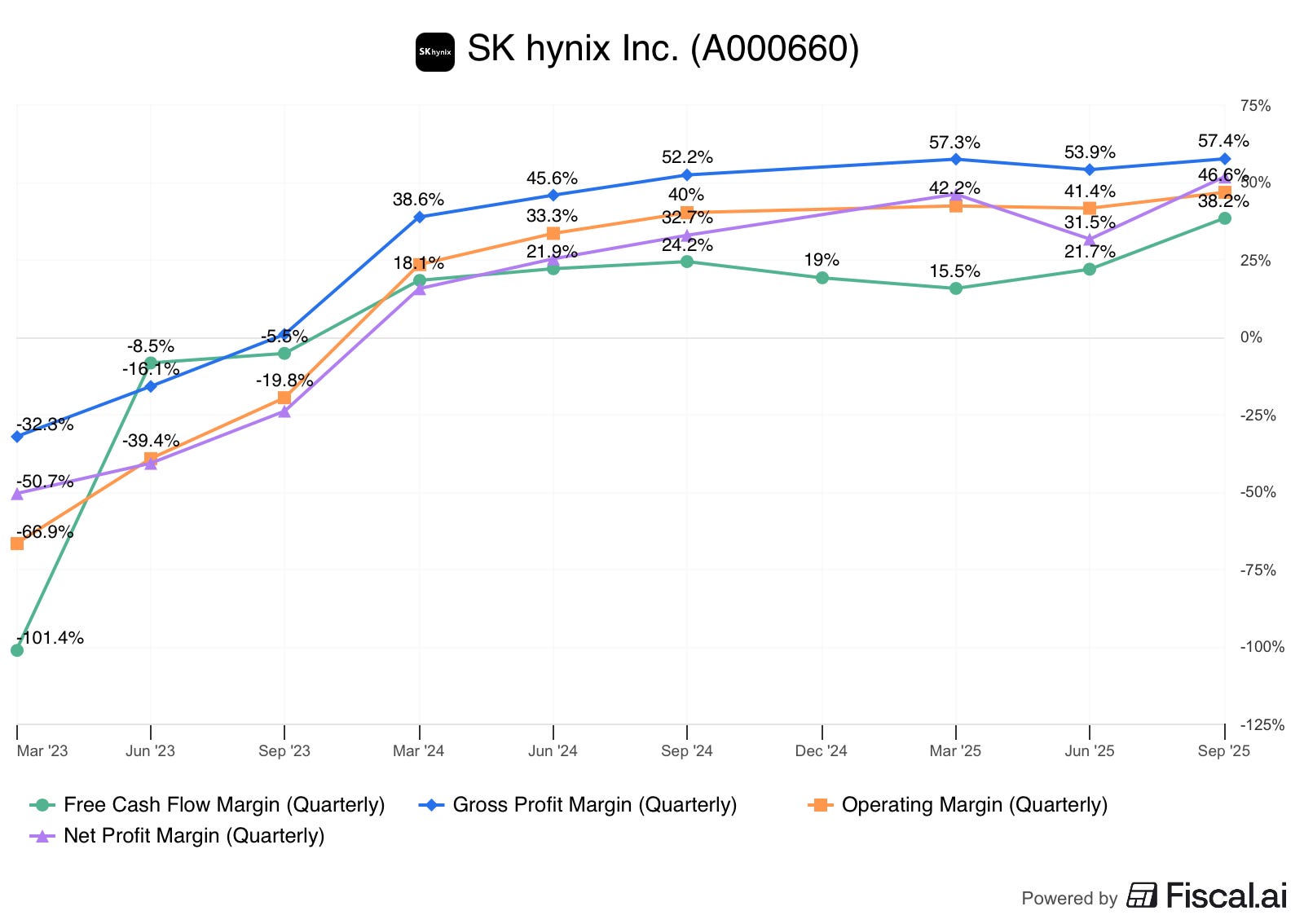

Margins

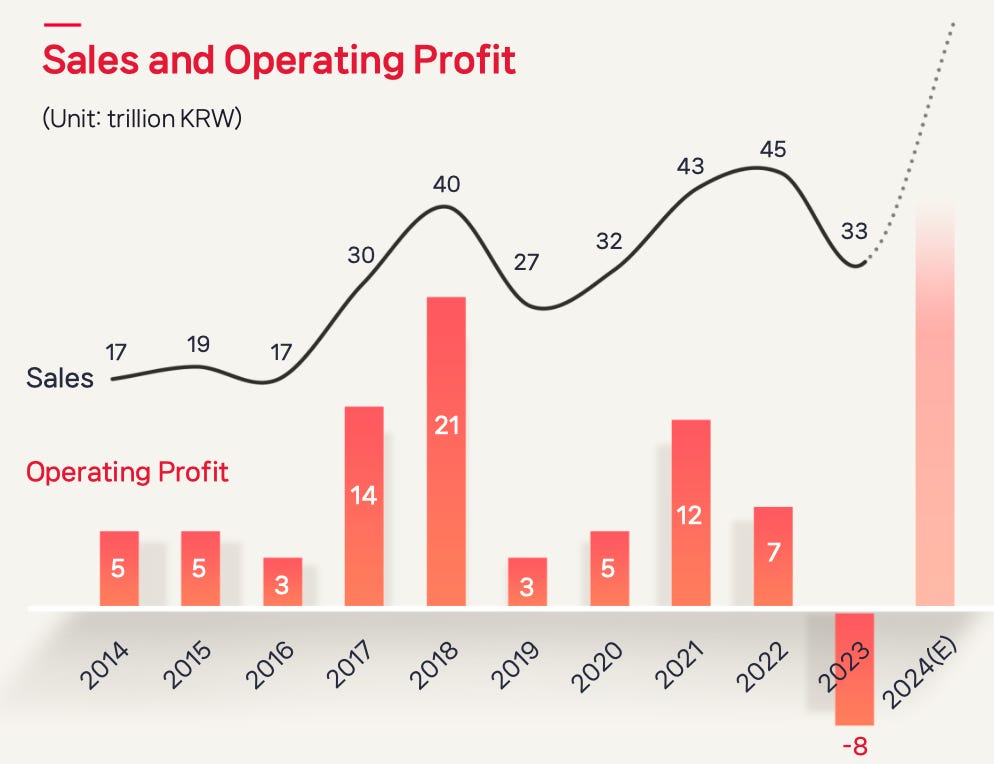

As we saw earlier, 2022 and 2023 were difficult years. After good years during COVID, sales were down in 2023 with an operating loss reported.

With such rapid revenue growth, operational leverage is now kicking in, driving margins significantly higher.

Net income margin in the last quarter reached an impressive 51.5%, slightly higher than operation profit. Free cash flow margin is also close to 40%. On the income statement, SK Hynix also reports equity investment and financial income. They saw a ₩3.3 trillion valuation gain on investment assets. Remember this gain is non-cash, it’s simply an adjustment to the fair value of their investments, so it’s counted outside of operating profit.

They haven’t released the full report from Q3, so we can’t really be sure where this come from. We do know from the Q2 that they have about ₩5.8T in long-term investment assets and ₩1.8T in equity investments. These equity investments are mostly concentrated in five core positions.

SK hynix System IC (Wuxi) - 50.1% | ₩622B

Joint venture producing system ICs (controllers, management chips) in Wuxi, China. Non-memory semiconductor manufacturing.SK China Company - 11.87% | ₩420B

Holding company for SK hynix’s operational footprint in China, likely including the Wuxi DRAM fab infrastructure.SK South East Asia Investment - 20.0% | ₩351B

Investment vehicle targeting tech companies and semiconductor ecosystem players across Southeast Asia growth markets.Others (Associates) - Various | ₩173B

Collection of smaller equity stakes in semiconductor-adjacent companies, likely including memory technology startups, equipment suppliers and AI tools.HITECH Semiconductor (Wuxi) - 45.0% | ₩132B

Joint venture for memory production in Wuxi, China. Likely legacy DRAM or NAND products for local market.

Equity investments and long-term investment assets accounted for roughly 2% of the market cap and over 5% of total equity (from Q2 numbers). These numbers are probably higher due to ₩3.3T readjustment in valuation as seen above.

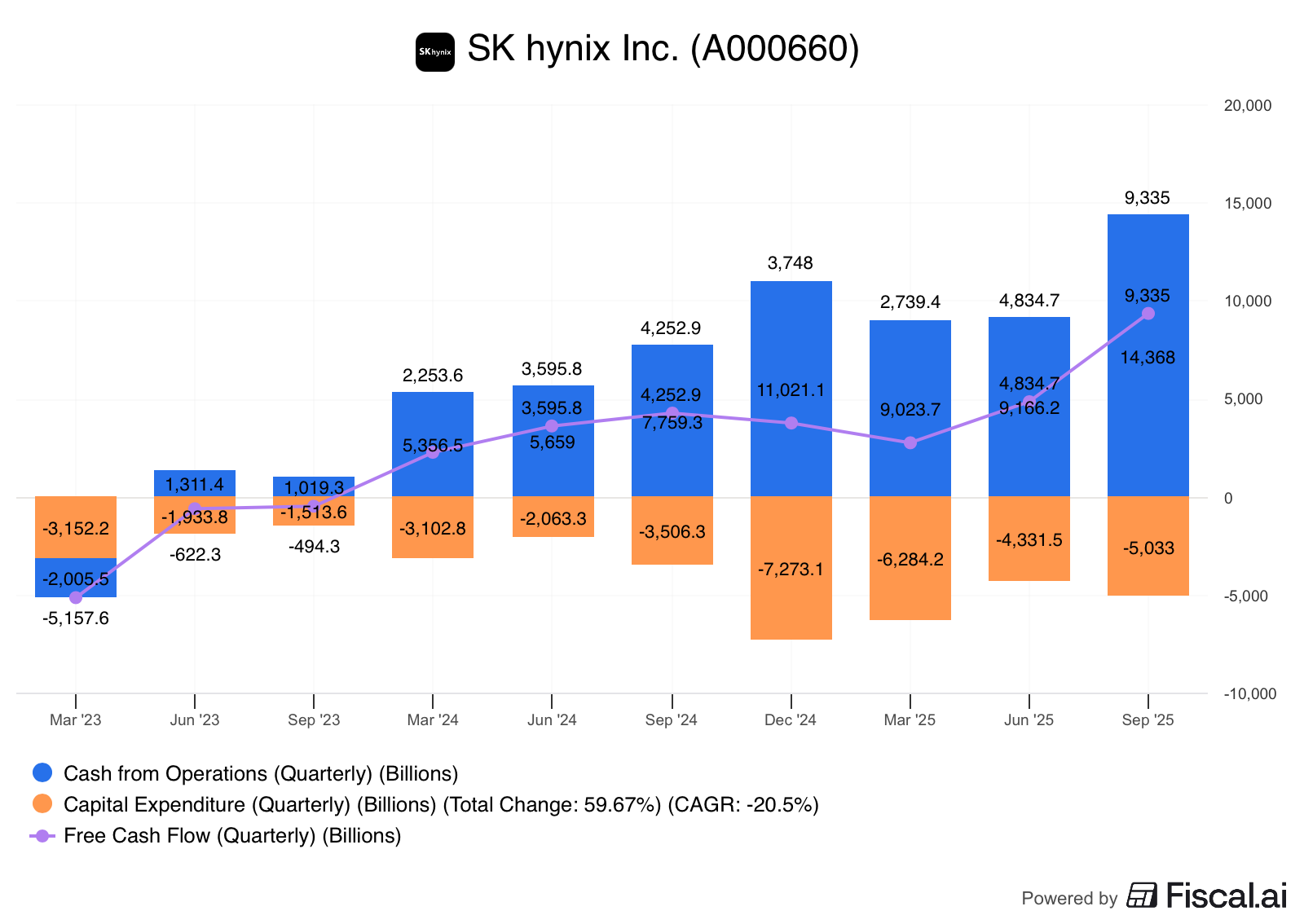

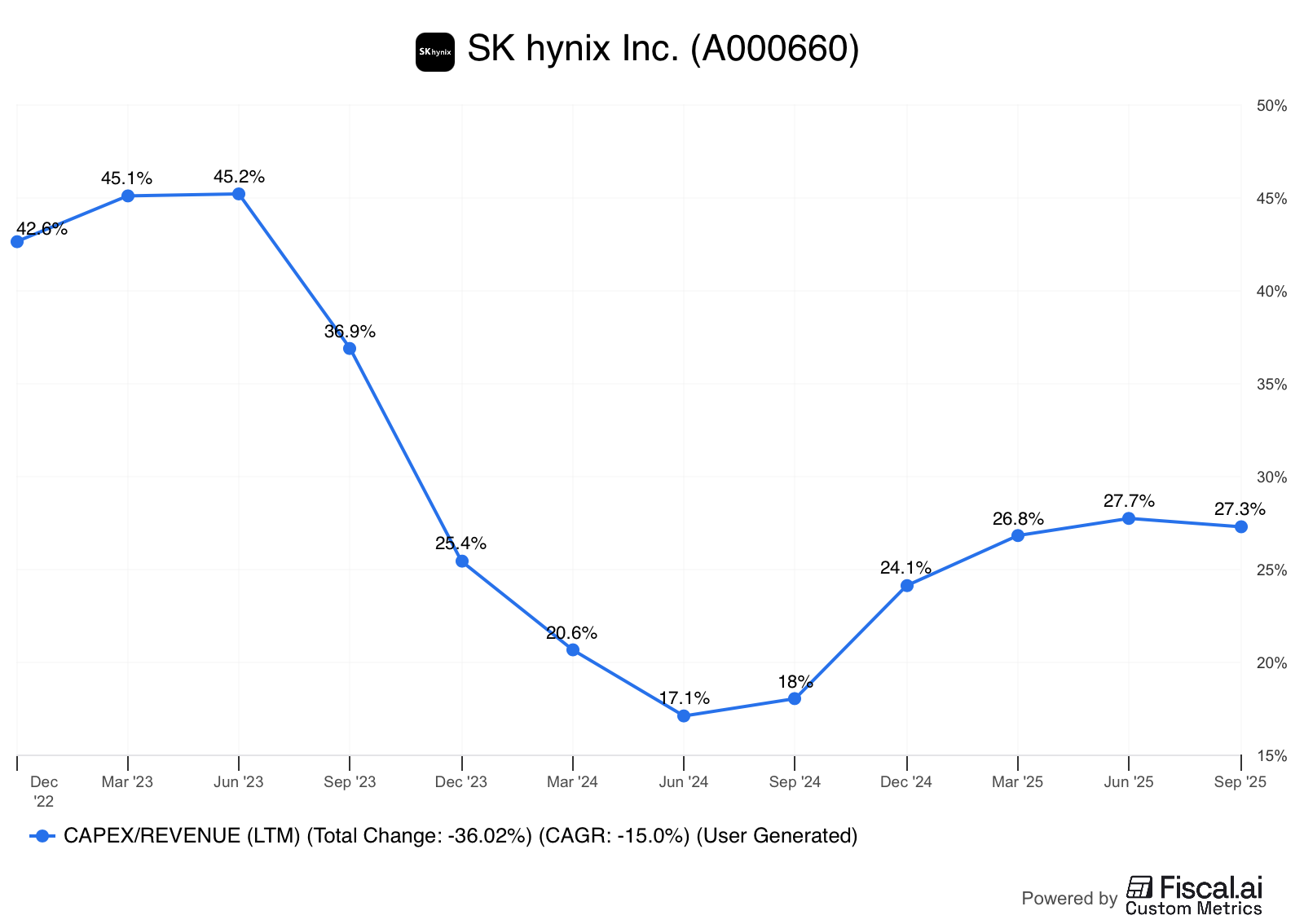

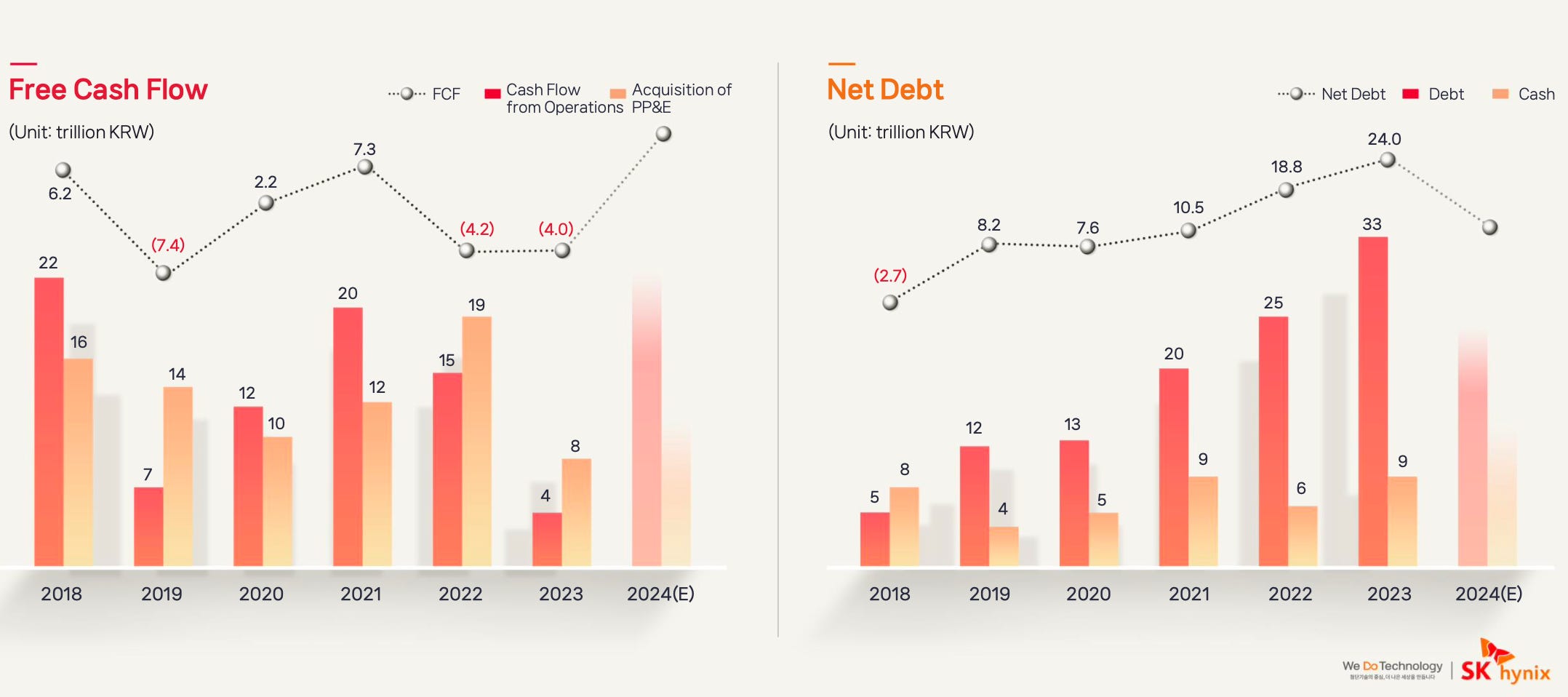

Free cash flow and CAPEX

Free cash flow, despite heavy investments have been positive since Q1 2024. Interesting to see that CAPEX was higher in the last quarter of last year followed by Q1 2025. Since then, it stabilised around ₩4-5T despite significant growth in revenues.

Management guided that in the future they expect CAPEX to be around 30% of the revenues.

Actually CAPEX has been slightly under 30%. As they launch new HMB’s, Capex will likely trend higher and be close to the 30% target. If we think that revenues are growing over 30%, the growth in CAPEX in absolute terms will rise sharply.

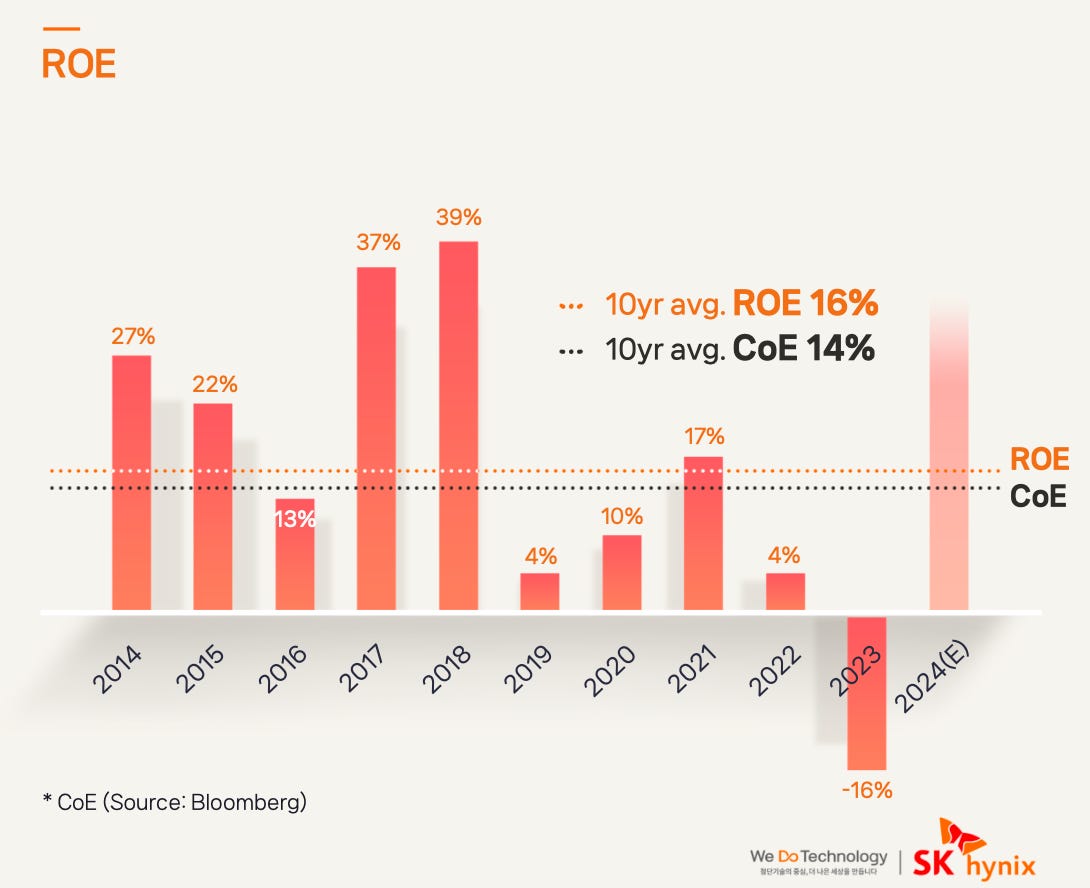

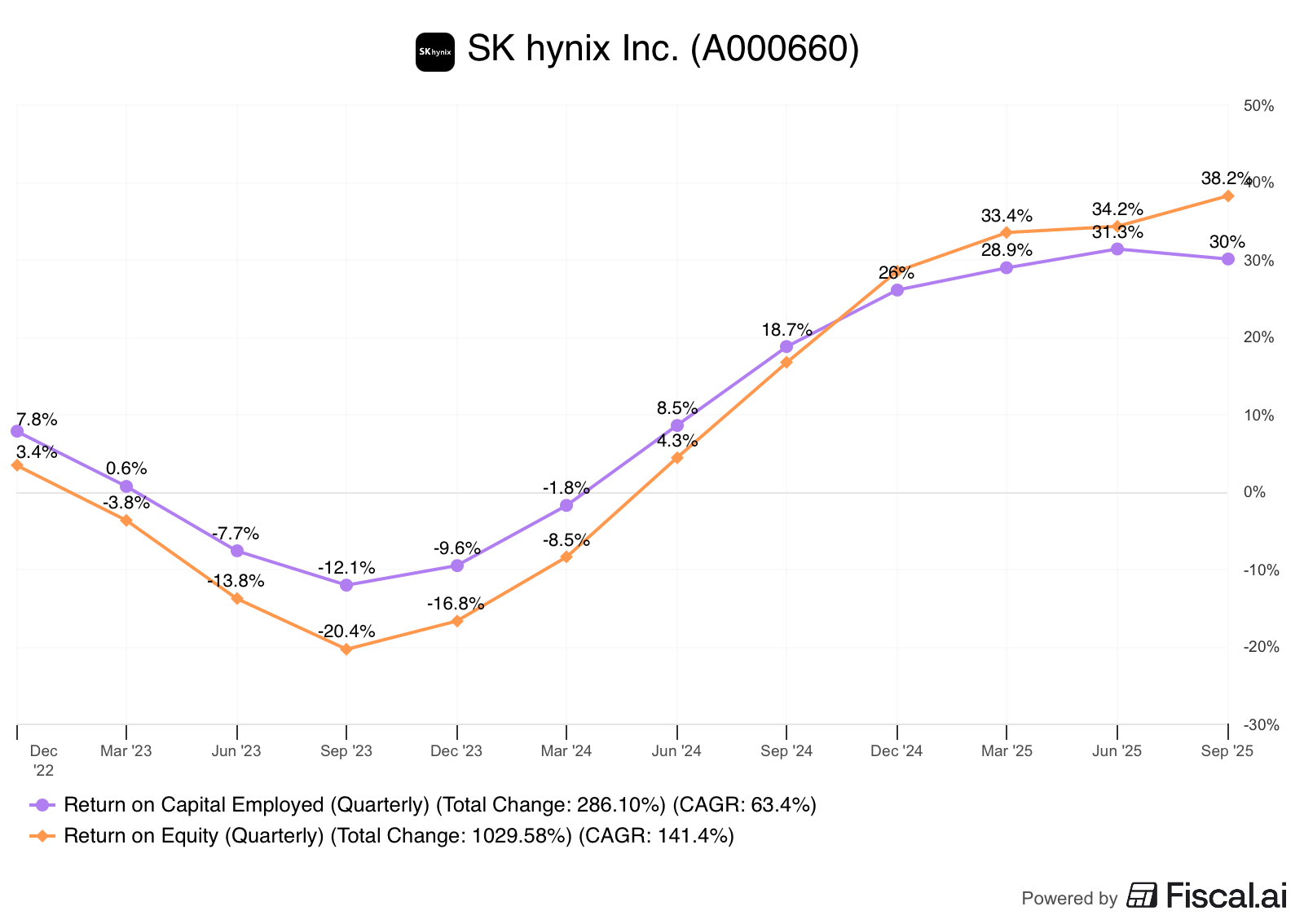

ROE

Return on equity has been averaging around16% with significant ups and downs due to cyclicality. This is 2% higher than the cost of capital (they use Cost of Equity). This is a key point, as they just create value for shareholder if they manage to have returns higher than the cost of capital.

This gap is way bigger now as they are having returns on equity close to 40%. ROCE is also been trending higher and sits around 30%, which is really good.

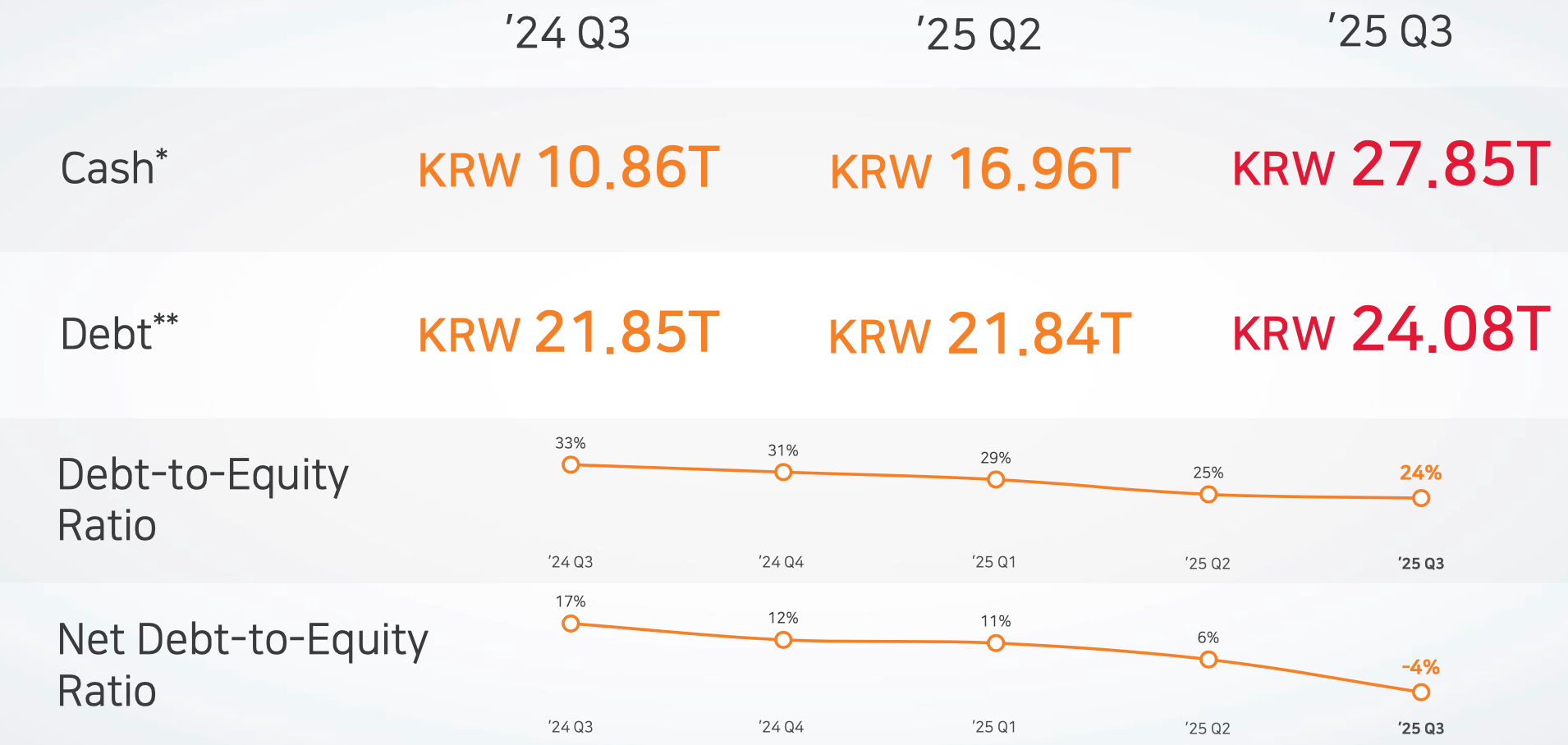

Debt

With such investments and being a capital intensity business, we need to pay attention to the debt levels. Debt peaked in 2023 as they went through heavy investments and M&A. In 2021 was a key year as they:

Started mass production of new gen DRAM

Developed world’s first HBM3

Acquired Solidigm

Last quarter there was a net cash position of nearly ₩4T, mainly due to increase in cash & cash equivalents. In one quarter alone they added over ₩10T in cash. Impressive! Future investment would probably rely on cash flows as they have been generating strong cash flow.

MOAT

Intangible Assets

SK Hynix’s most formidable asset is not its factories, but the patented technology and specialized know-how that makes its products indispensable.

The clearest example is their dominance in HBM. SK Hynix was the first to successfully mass-produce advanced HBM generations (HBM3, HBM3E) and holds key patents for the crucial vertical stacking and testing processes.

This technological lead grants them a powerful intangible asset: a reputation for irreplaceable quality. Companies like NVIDIA, are critically dependent on SK Hynix for HBM supply. This dependency allows SK Hynix to command premium pricing and achieve high profit margins, even during market downturns, something commodity producers cannot do.

Efficient Scale

The memory market requires capital on an astronomical scale, which creates a powerful moat of Efficient Scale for SK Hynix.

The cost to design, build, and equip a single modern semiconductor fabrication plant (“fab”) can easily exceed $10B. This barrier to entry is so high that it effectively prevents new competitors from entering the DRAM and HBM markets. The cost and risk are simply too great.

The advanced nature of HBM production means that even among existing competitors (Samsung, Micron), only a few possess the technical expertise and established scale to deliver it reliably.

By leveraging these two moats, their exclusive HBM technology and the scale of their manufacturing base, SK Hynix has built a strong defence around its market share, positioning itself as a central, indispensable player in the future of AI.

Risks

While SK Hynix has strong competitive moats, the company operates in the volatile semiconductor industry, exposing investors to several risks. These risks center on market cycles, technological disruption, and geopolitical factors.

Cyclicality and Commodity Pricing

The most prominent risk in the memory sector is cyclicality. The DRAM and NAND markets are notoriously cyclical, often oscillating wildly between periods of high profits and periods of severe losses.

When demand exceeds supply, prices skyrocket, leading to high profitability (as seen with HBM today). However, when too much manufacturing capacity is brought, the market quickly flips into a period of oversupply, causing prices to crash.

During downturns, SK Hynix accumulates large inventories. Its massive operating scale means any market downturn can lead to steep, sudden losses due to the high fixed costs of running multi-billion dollar fabrication plants, like those we saw in 2023.

Technological Obsolescence and CAPEX Burden

The company’s core business relies on continuous, aggressive innovation, which carries inherent risks.

SK Hynix must constantly spend billions of dollars in CAPEX and R&D simply to keep pace with rivals Samsung and Micron. Failure to master the next process node or the next HBM means losing market share and technological leadership.

While HBM is currently a massive strength, it is also a risk. If a rival finds a way to deliver similar bandwidth without the complexity and cost of HBM’s vertical stacking, the value of SK Hynix’s specialised HBM could be hammered quickly.

Geopolitical and Regulatory Exposure

As a South Korean technology giant, SK Hynix is highly exposed to global political dynamics, particularly concerning the US and China.

The company has massive manufacturing operations in China and depends on the Chinese market for a significant portion of its revenue. Tensions (such as US-led export controls on advanced chip-making equipment) directly affect SK Hynix’s ability to operate and upgrade its Chinese facilities, forcing costly adjustments to its supply chain.

SK Hynix relies on a handful of specialised suppliers (like ASML for EUV lithography) located in different countries. Any disruption can halt production globally.

Competition and Pricing Pressure

Despite the HBM moat, the broader DRAM and NAND markets are highly competitive commodity spaces dominated by only three players.

Except for specialised products like HBM, DRAM and NAND are largely commodities (pricing is driven by the cheapest producer). Fierce competition with Samsung and Micron limits SK Hynix’s ability to consistently raise prices for conventional memory.

Both Samsung and Micron are aggressively investing to close the HBM gap. If they successfully match SK Hynix’s technology in HBM4 or HBM5, the company’s current pricing premium and market leadership will be eroded, making HBM a commodity.

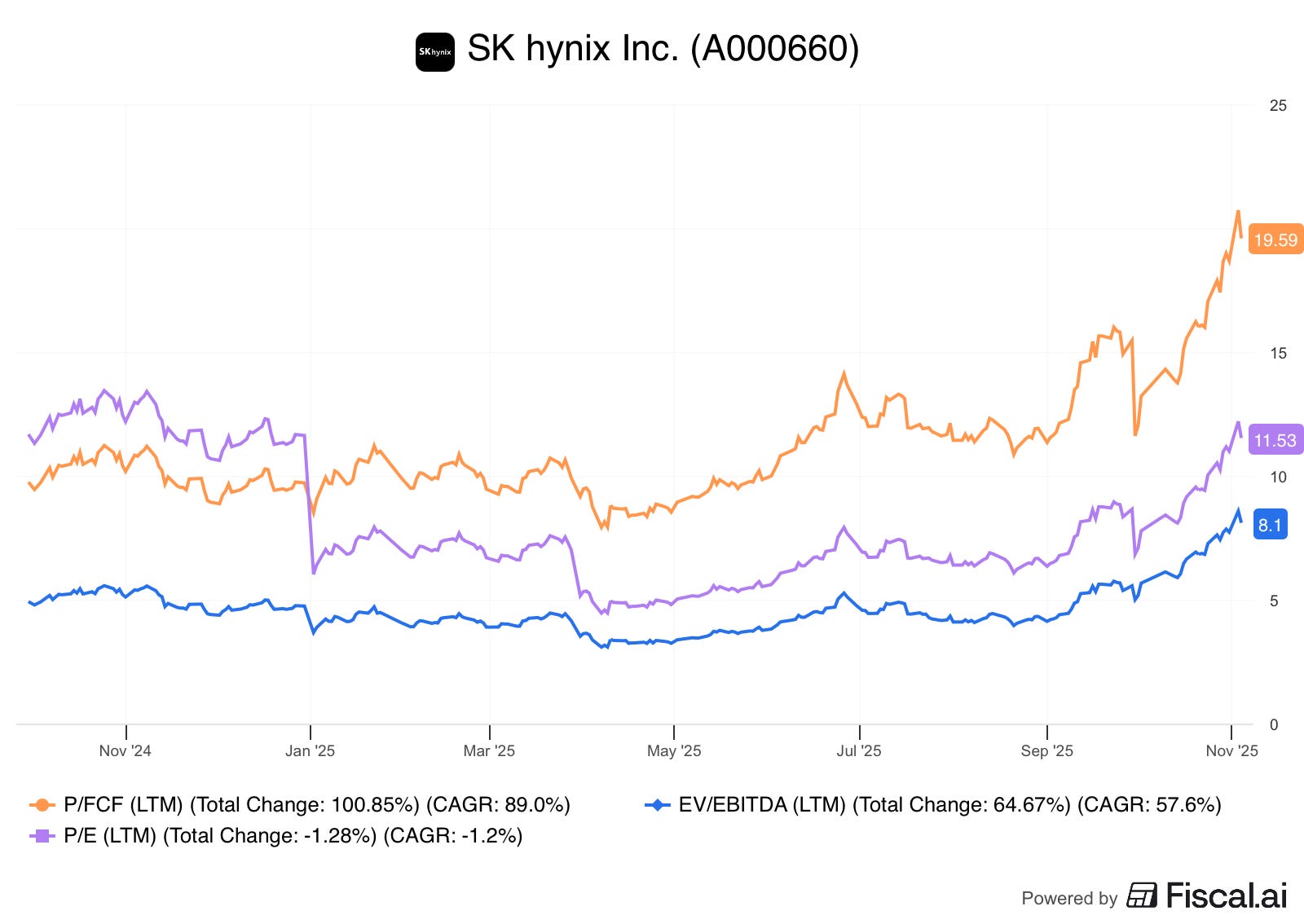

Valuation

South Korean companies usually trade at much lower multiples than those in the U.S. or Europe for a few reasons: the tension with North Korea, complex ownership structures, weak protection for small shareholders, and decisions that often lack transparency. The Korean stock market is also less liquid and accessible compared with the US or even Europe.

That said, lets look at a few valuations multiples:

Anywhere you look, SK hynix doesn’t look expensive even with a P/FCF around 20. Yet the stock has surged nearly +195% YTD, showing just how absurdly cheap it was earlier this year. It’s hard to believe in the fact that a company like this, even in a cyclical industry, was trading at a single-digit P/E not long ago.

Sure, it’s a Korean company, but that alone doesn’t justify how undervalued it was. We’re talking about a business that plays a critical role in AI infrastructure with more than half of the world’s GPUs using SK Hynix memory technology.

Future investments

As we’ve already discussed, demand for DRAM, especially for high-performance products like HBM is soaring. SK hynix continues to innovate and is preparing to roll out its next-generation HBM4, a major upgrade over HBM3. With higher bandwidth and greater efficiency, it will enable faster AI model training. And according to management, it’s already sold out through 2026:

’’Meanwhile, the company has completed discussions with key customers regarding HBM supply for next year. HBM4, which completed development in September and entered mass production, fully meets customer performance requirements and supports industry-leading speeds. Shipments will begin in the fourth quarter this year, with full-scale sales expansion planned for next year.’’

‘‘Secured customer demand across all DRAM, NAND products including HBM through Yr. ‘26’’

Not just the HBM, but also NAND and all DRAM.

To meet this surging in demand, SK Hynix is expanding production in its M15X fab in Cheongju, where equipment installation is already underway. The company is also investing heavily in the US, around ₩5.3T ($3.9B) to build an advanced HBM packaging and R&D facility in Indiana. It’s the first advanced packaging project for AI products on American soil, aim to bring SK hynix closer to its key US clients like NVIDIA, improving logistics and potentially reducing costs.Production is expected to start in 2028.

While HBM dominates the growth story, SK Hynix continues advancing its core DRAM and NAND businesses to maintain leadership across the full memory portfolio.

In DRAM, the company is accelerating migration to its most advanced 1cnm manufacturing process throughout 2026, offering better efficiency and lower costs. This supports growing demand for high-performance memory in data centers and AI systems while maintaining competitive advantages against Samsung and Micron.

In NAND, SK hynix is ramping production of 321-layer flash memory, the industry’s highest layer count with focus on enterprise SSDs for AI servers and data centers. The company is investing to expand capacity by 2026, shifting away from commodity consumer products toward higher-margin enterprise applications where AI workloads demand greater capacity and reliability.

Investment thesis

We know that SK Hynix plays a crucial role in AI thanks to its advanced memory technology. It’s the largest DRAM manufacturer, ahead of Samsung and Micron, producing over one-third of the world’s DRAM. This production is mainly driven by its HBM technology, which powers GPUs like those used by NVIDIA (and we all know how NVIDIA has been struggling with supply shortages)

But SK Hynix isn’t just about DRAM. It’s also a key player in NAND, the chips used in SSDs. With the acquisition of Intel’s NAND and SSD business, the company jumped to #2 in global market share, holding about 20% versus Samsung’s 32%.

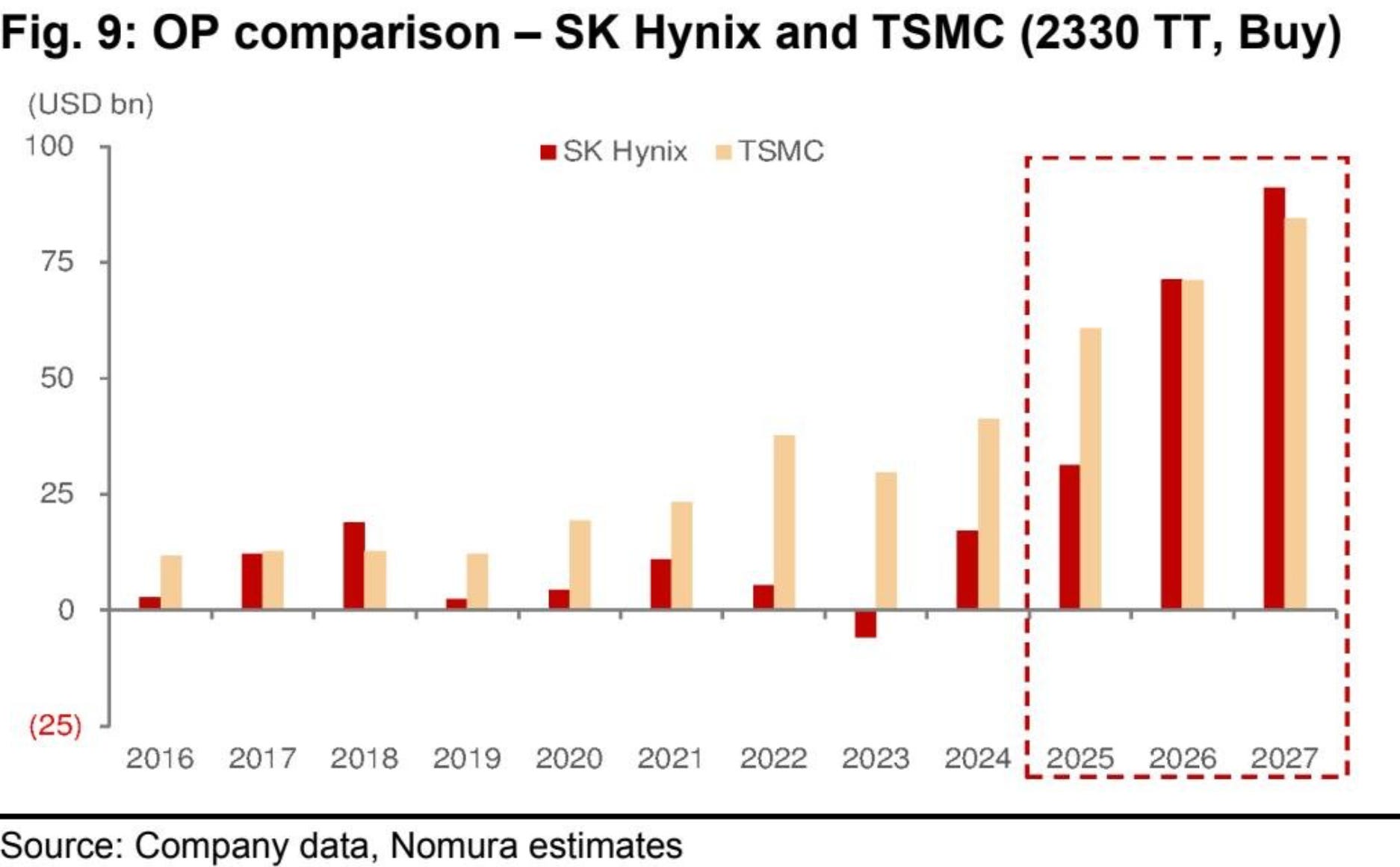

Some analysts and investors have been rising their forecast for revenues, margins, and operating profits. Nomura, a major Japanese investment bank, predicts that SK Hynix will generate more operating profit than TSMC in 2027, an interesting projection considering that TSMC is the world’s largest semiconductor foundry (manufactures chips for Apple, NVIDIA, and AMD).

To give you some perspective, today TSMC is worth 4x more than SK hynix ($1,200B vs $302B). TSMC is one of the most important companies in the world when it comes to semiconductors, yet SK Hynix is also critically relevant. If Nomura is right, SK Hynix could easily double its current valuation.

According to SK Hynix last quarterly report, demand for DRAM and NAND will be growing even faster in 2026, with over 20% for DRAM (most likely due to HBM) and high teens for NAND.

So, there’t no signs of things slowing down.

Projections

SK Hynix has been raising revenues well over 30%. Although demand is skyrocketing with no signs of slowing down, and the new HBM is pricier than the older HBM3, there’s still significant room for margin improvement. On the other hand, the company is rapidly reaching full capacity. Given that some of the major capital investments currently being made will only be ready in a couple of years, revenue growth may be constrained, not due to falling prices or fading demand, but simply because there isn’t enough supply to meet the demand.

To be conservative on SK Hynix’s long-term valuation, let’s model the company using a 25% revenue CAGR over the next five years. We will also maintain a FCF margin of 25% (consistent with the last twelve months), although this is likely to be higher given the company’s pricing power.

Under these conservative assumptions, SK Hynix would achieve ₩250T in revenue and ₩63T in FCF in 5 years.

A company like this in the US would likely trade at an exit multiple of +30x. However, we know that South Korean companies typically trade at a discount, so we will apply a conservative P/FCF multiple of 17x.

Applying a 17x multiple to the ₩63T FCF we get a market capitalisation close to ₩1,100T.

Assuming 1% dilution over that period, this translates to a final estimated stock price of ₩1,460.

At today’s price, this scenario suggests a potential CAGR of close to 20%. Once again, I believe these projections, 25% revenue growth, 25% FCF margin, and 17x exit multiple are likely too conservative. I would not be surprised if SK Hynix reached the ₩63T FCF target in just 3–4 years. If they manage to achieve that, the market would almost certainly reward them with an exit multiple of +20x.

Every valuation method we use leads us to the same conclusion: SK Hynix appears to be extremely cheap.

Looking at the numbers, everything looks perfect, but we can’t forget that there are still risks. We should’t forget the cyclicality of the semiconductor business and also the exposure to geopolitical risks given its proximity to North Korea and its significant business relationship with China.

Korea Exchange

I haven’t mentioned a very important point: most brokers don’t let us invest directly in Korea, which might be one reason SK hynix trades at such low valuations. Fortunately, there’s another way: SK hynix also trades on Germany’s Xetra exchange under the ticker HY9H as a German Depositary Receipt (GDR), which is similar to a US ADR (like BABA). This allow us to buy SK hynix in euros without needing a Korean brokerage account.

A GDR is basically a certificate issued by a German bank that holds the actual Korean shares. This means we get the economic ownership of the stock without the hassle of opening a Korean account or dealing with currency conversion.

The problem here is liquidity is very low and this leads to wider spreads and less efficiency. For small investments, it might be fine, but for larger positions, the low liquidity can be a big problem.

Also, the GDR price can sometimes drift away from the Korean share price due to thin trading, and dividends may face withholding taxes in both Korea and Germany (though tax treaties often allow you to reclaim some).

In short, Xetra GDRs might be convenient for small investors who can’t access the Korean market. But for larger investments, buying directly on the Korean Exchange is much better because of liquidity, tighter spreads, and better execution.

Disclaimer: The views and opinions expressed here are my own and are shared for educational and informational purposes only. This content is not financial advice and should not be interpreted as a recommendation. I currently hold a position in SK Hynix.

Couldn't agree more. It's truely fascinating how much hardware like HBM underpins the AI advancements I read about; I wonder how companies manage to predict what technology will become so crucial years in advance?